Beginner-Friendly Walkthrough for Applying for Equity Release Mortgages

Beginner-Friendly Walkthrough for Applying for Equity Release Mortgages

Blog Article

Exactly How Equity Release Mortgages Can Influence Your Financial Future and Retired Life Plans

Equity Release home mortgages present both opportunities and challenges for individuals planning their monetary futures and retired life. They can offer prompt liquidity, easing the problem of living expenditures. These products likewise lessen the worth of estates, impacting inheritance for heirs. Comprehending the subtleties of equity Release is important. As people explore their options, they need to take into consideration the wider implications on their monetary wellness and legacy. What choices will they encounter in this complicated landscape?

Comprehending Equity Release Mortgages: What You Need to Know

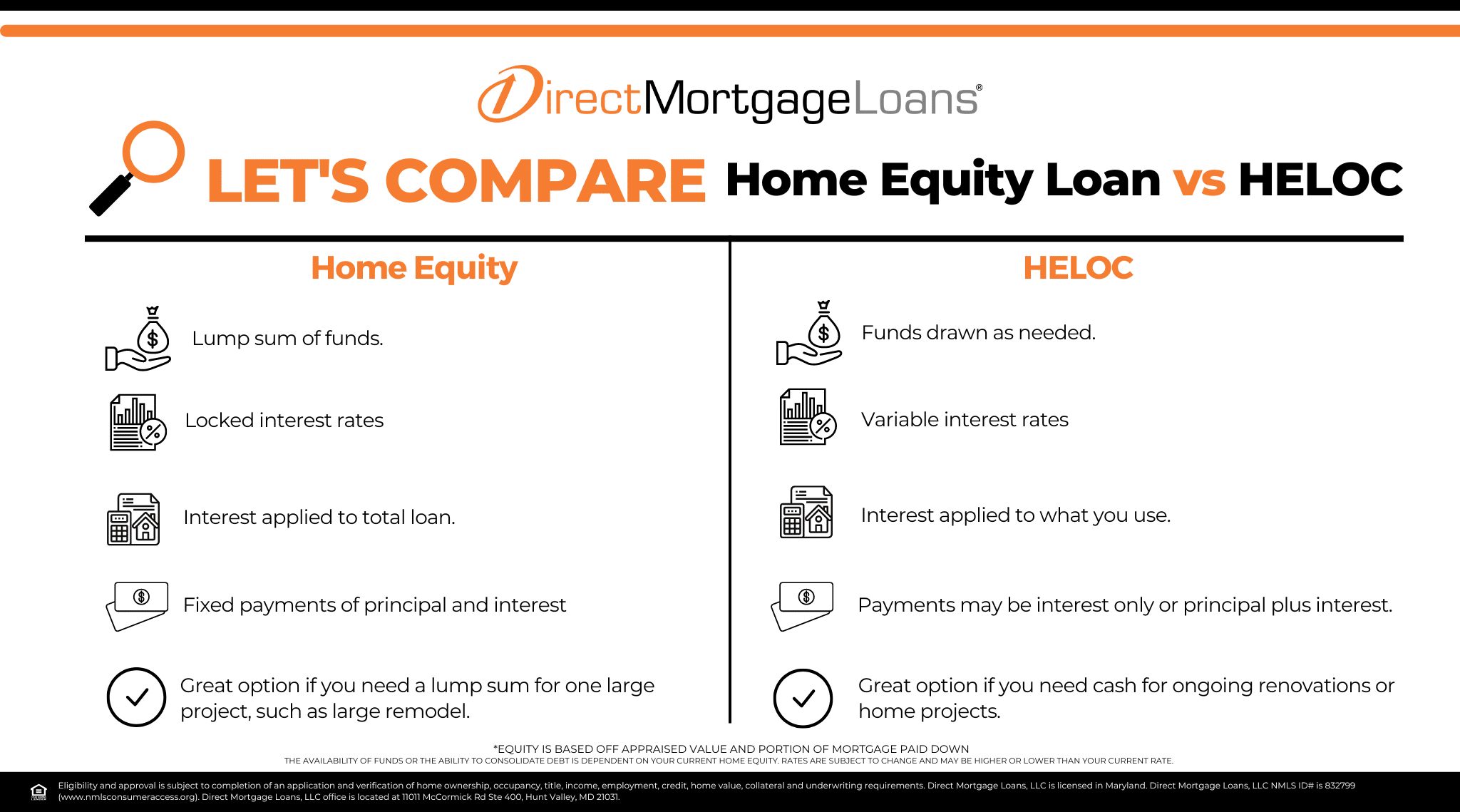

Types of Equity Release Products Available

Equity Release products can be found in numerous forms, dealing with various demands and choices of property owners. Both key types are life time home mortgages and home reversion plans.Lifetime mortgages enable house owners to obtain versus their property while keeping possession. The lending, plus passion, is generally paid off upon fatality or when the home is marketed. This alternative supplies adaptability and permits continued home in the home.Conversely, home reversion intends entail marketing a portion of the building to a supplier in exchange for a swelling amount or routine settlements. The property owner maintains the right to live in the home up until they pass away, but the copyright gains possession of the marketed share.Both products have one-of-a-kind benefits and considerations, making it essential for individuals to examine their monetary scenarios and lasting goals before proceeding. Understanding these options is important for notified decision-making relating to equity Release.

How Equity Release Can Offer Financial Alleviation in Retired Life

Immediate Cash Money Accessibility

Several retirees face the obstacle of handling fixed incomes while steering rising living expenses, making instant cash accessibility an essential factor to consider. Equity Release mortgages supply an efficient option, allowing property owners to access the value of their residential or commercial properties without the demand to offer. This economic device allows retired people to access a swelling sum or regular payments, supplying them with the needed funds for day-to-day costs, unanticipated costs, or even leisure tasks. By touching into their home equity, retired people can minimize monetary anxiety, preserve a comfy way of life, and preserve their cost savings for emergency situations. Immediate cash accessibility with equity Release not just improves monetary flexibility but likewise empowers retired people to enjoy their retired life years with better comfort, complimentary from prompt monetary restraints.

Debt Debt Consolidation Benefits

Accessing prompt cash can significantly enhance a senior citizen's monetary circumstance, yet it can also function as a critical device for taking care of existing financial debts. Equity Release home loans supply a possibility for senior citizens to touch right into their home equity, offering funds that can be made use of to consolidate high-interest debts. By repaying these financial debts, retired people may decrease month-to-month financial problems, enabling a much more workable spending plan. This strategy not only simplifies finances yet can also boost total monetary security. Furthermore, the cash money obtained can be alloted towards essential expenditures or investments, further supporting retirement. Inevitably, using equity Release for debt consolidation can lead to considerable lasting financial relief, enabling retirees to appreciate their gold years with higher peace of mind.

The Effect of Equity Release on Inheritance and Estate Preparation

The choice to use equity Release can considerably alter the landscape of inheritance and estate planning for individuals and their family members. By accessing a part of their home's value, homeowners may considerably lower the equity available to hand down to successors. This option can produce a complicated dynamic, as people have to evaluate prompt monetary demands against lasting heritage goals.Moreover, the funds launched through equity can be utilized for numerous purposes, such as enhancing retirement you can try these out way of livings or covering unforeseen expenses, but this usually comes at the cost of future inheritance. Households might encounter challenging discussions regarding expectations and the effects of equity Release on their monetary legacy.Additionally, the obligations linked to equity Release, such as repayment conditions and the possibility for diminishing estate value, need cautious factor to consider. Ultimately, equity Release can improve not only monetary circumstances however also family members connections and assumptions surrounding inheritance.

Tax Obligation Ramifications of Equity Release Mortgages

The tax implications of equity Release home loans are crucial for home owners considering this alternative. Specifically, resources gains tax obligation and inheritance tax obligation can significantly impact the financial landscape for individuals and their heirs (equity release mortgages). Understanding these considerations is vital for efficient monetary planning and monitoring

Funding Gains Tax Considerations

While equity Release mortgages can give homeowners with instant monetary relief, they additionally bring potential tax effects that have to be carefully taken into consideration. One essential aspect is resources gains tax (CGT) When a house owner releases equity from their home, they may face CGT if the property value rises and they decide to market it in the future. The gain, which is computed as the difference in between the market price and the original purchase price, goes through tax. Home owners can profit from the main residence alleviation, which may exempt a section of the gain if the residential property was their main home. Recognizing these subtleties is vital for property owners planning their monetary future and examining the long-lasting impact of equity Release.

Inheritance Tax Implications

Taking into consideration the prospective effects of inheritance tax is vital for homeowners opting for equity Release home mortgages. When house owners Release equity from their residential or commercial property, the amount withdrawn might impact the value of their estate, possibly enhancing their estate tax responsibility. In the UK, estates valued over the nil-rate band limit go through inheritance tax at 40%. Therefore, if a house owner makes use of equity Release to money their retired life or other expenditures, the continuing to be estate could considerably lower, affecting beneficiaries. House owners need to think about the timing of equity Release, as early withdrawals might lead to greater tax effects upon fatality. Comprehending these aspects is important for effective estate planning and making sure that beneficiaries receive their designated legacy.

Analyzing the Dangers and Advantages of Equity Release

Equity Release can supply substantial economic advantages for homeowners, yet it is necessary to review the associated threats before continuing. One of the primary advantages is the capacity to gain access to tax-free cash money, making it possible for individuals to money their retired life, make home enhancements, or aid member of the family financially. The ramifications on inheritance are considerable, as launching equity reduces the value of the estate passed on to heirs.Additionally, interest prices on equity Release products can be higher than typical mortgages, leading to increased financial debt over time. Homeowners should also take into consideration the prospective effect on means-tested advantages, as accessing funds might impact qualification. Moreover, the complexity of equity Release items can make it challenging to comprehend their long-term implications totally. Therefore, while equity Release can offer instant monetary relief, a detailed assessment of its risks and benefits is vital for making educated decisions about one's financial future

Making Informed Decisions Concerning Your Financial Future

Homeowners deal with a plethora of options when it involves handling their financial futures, particularly after pondering choices like equity Release. Educated decision-making is vital, as these selections can significantly influence retirement and overall monetary health and wellness. Homeowners ought to begin by extensively looking into the implications of equity Release, consisting of prospective influence on inheritance and future care costs. Involving with monetary advisors can provide customized insights, allowing individuals to recognize the lasting consequences of their decisions.Moreover, house owners must think about alternative choices, such as scaling down or various other types of funding, to establish the most ideal course. Examining one's economic situation, consisting of properties and debts, is crucial for making a versatile choice. Inevitably, a mindful evaluation of all available options will certainly empower house owners to navigate their economic futures confidently, ensuring they align with their retired life objectives and personal ambitions.

Often Asked Questions

Can I Still Move Home if I Have an Equity Release Mortgage?

The person can move home with an equity Release home loan, yet you can try here should comply with details lending institution problems. This often entails paying back the existing mortgage, which could impact their financial scenario and future strategies.

Just How Does Equity Release Affect My State Benefits Eligibility?

Equity why not try here Release can influence state benefits qualification by increasing assessable earnings or resources. Consequently, individuals may experience decreases in advantages such as Pension Credit Score or Housing Benefit, possibly influencing their general financial backing throughout retirement.

What Occurs if I Outlast My Equity Release Plan?

If a specific outlives their equity Release plan, the home mortgage normally continues to be basically until their passing away or relocating into lasting care. The estate will be liable for clearing up the financial obligation from the building's value.

Can I Repay My Equity Release Home Loan Early?

Repaying an equity Release home loan very early is typically feasible but might entail fees or charges. Consumers should consult their lending institution for particular terms, as each strategy varies in conditions relating to early settlement options.

Are There Age Limitations for Obtaining Equity Release?

Equity Release generally imposes age restrictions, usually needing applicants to be at the very least 55 or 60 years old. These limitations ensure that people are coming close to retired life, making the system a lot more suitable for their financial circumstance.

Conclusion

In recap, equity Release mortgages supply a potential monetary lifeline for retirees, giving instant money access to improve quality of life. They come with substantial factors to consider, consisting of influences on inheritance, estate preparation, and tax responsibilities. Thoroughly examining the risks and benefits is vital for ensuring that such choices straighten with lasting economic objectives. Consulting with a monetary consultant can aid individuals navigate these intricacies, ultimately sustaining an extra protected and enlightened financial future. Equity Release home loans are monetary items developed for home owners, usually aged 55 and over, enabling them to access the equity tied up in their residential or commercial property. Equity Release home loans give a possibility for retired people to tap right into their home equity, offering funds that can be used to consolidate high-interest debts. Households might face hard conversations pertaining to expectations and the implications of equity Release on their monetary legacy.Additionally, the responsibilities linked to equity Release, such as repayment conditions and the possibility for reducing estate value, call for careful factor to consider. While equity Release mortgages can supply homeowners with instant economic alleviation, they also bring possible tax ramifications that must be carefully taken into consideration. The effects on inheritance are considerable, as releasing equity reduces the worth of the estate passed on to heirs.Additionally, interest prices on equity Release products can be higher than traditional home loans, leading to increased financial obligation over time.

Report this page